Marginal Tax Rates: How the Progressive Tax System Really Works

- Gin

- Nov 28, 2025

- 4 min read

Updated: Dec 3, 2025

(and why getting bumped into a higher tax bracket isn’t the disaster people think it is)

In my previous post, I mentioned that capital gains and dividends can fall within a zero percent tax bracket if you hold your investments long enough. Imagine: legally not having to pay taxes on thousands of dollars of income. Cha-ching!

But before we get that fun part—we need to clear up one thing: how our progressive income tax system works. Many people misunderstand how ordinary income is taxed—and that misunderstanding costs people real money.

So, let’s clear up the confusion.

THE MYTH: A HIGHER TAX BRACKET TAXES ALL OF MY INCOME

You may have heard some version of:

“If I make too much, I’ll get bumped into a higher tax bracket and lose money.”

I’ve met people who genuinely believed that if they crossed even one dollar into a higher tax bracket, suddenly all their income would be taxed at that higher rate. As if the IRS is just waiting to snatch away their entire paycheck if they slip up.

Good news: that’s not how any of this works. The IRS may be more Grinch than Santa Claus, but it doesn’t punish you for earning more money. This is because our tax system uses marginal tax rates.

If talk about progressive taxes and marginal rates makes your head hurt, don’t worry — it’s actually pretty easy to understand. Let’s jump in.

WHAT IS A PROGRESSIVE TAX SYSTEM?

The United States has a progressive income tax system. All this means is:

Different parts of your income get taxed at different rates

The higher your income, the higher the rate on the top slice

No, your entire income does not suddenly get taxed at the highest bracket you touch

You can be in the 22% tax bracket without paying 22% on every dollar. If earning $48,476 meant paying 22% on all $48,476 just because you earned one extra dollar… well, that would really suck. Fortunately, that’s not how it works.

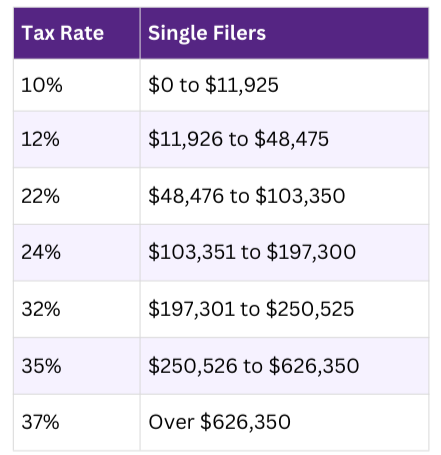

Here are the 2025 tax brackets for single filers:

You'll notice the big jumps, especially from the 12% to 22% tax brackets. But those jumps don't punish your previous dollars.

That's where marginal tax rates come in.

HOW MARGINAL TAX RATES WORK

(aka, the part nobody taught us in school)

Marginal tax rates sound intimidating, but they’re not. They simply mean: Only the portion of your income that falls within each bracket is taxed at that bracket’s rate.

Let’s look at how $60,000 of income is taxed.

An income of $60,000 would technically put you “in” the 22% bracket. But notice that the entire $60,000 doesn’t fall within the 22% range. Your income spans across the 10% and 12% brackets first.

Here’s how it breaks down:

First $11,925 taxed at 10%

Next $36,550 (from $11,926 to $48,475) taxed at 12%

Final $11,525 (from $48,476 to $60,000) taxed at 22%

Broken down:

$11,925 × 10% = $1,192.50

$36,550 × 12% = $4,386.00

$11,525 × 22% = $2,535.50

Total tax: $8,114

That’s an effective tax rate of about 13.5% — not 22%.

A tax rate of 13.5% still isn’t pleasant, but it sucks a lot less than paying 22% across the board. Thank goodness for marginal tax rates.

WHY THE TAX BRACKET MISUNDERSTANDING IS COSTLY

If you’ve misunderstood how tax brackets work, you’re not alone. It’s extremely common. Nobody ever teaches us how our taxes are actually calculated. We just wait until tax season and hope the software doesn’t flash an error message that looks like a cry for help.

I watched a YouTube video recently of a woman proudly explaining how she turned down salary raises because she thought it would bump her into a higher bracket and reduce her take-home pay. She genuinely believed she was avoiding a financial penalty.

Except… she wasn’t.

She missed out on potentially thousands of dollars because of this misunderstanding. And I’m sure her employer didn’t rush to correct her — that would be like walking away from a poker game when you’ve just spotted the sucker at the table.

If her employer loved her enough to offer a raise, they loved her even more when she turned it down. A great employee and doesn’t want to be paid more? That’s Employee of the Year!

But I know you won’t make the same mistake. You now know how marginal tax rates work — and how to calculate your effective tax rate.

If someone offers you a raise, take it. Mo’ money is mo’ money.

FINAL TAKEAWAYS ON MARGINAL TAX RATES

Our income tax system is confusing enough that entire careers exist to help people navigate it. But progressive tax brackets themselves? Surprisingly simple.

Now you know:

You never get taxed on all of your income at the highest bracket you touch

Marginal tax rates only apply to the dollars in each bracket

Your actual (effective) tax rate is almost always lower

Turning down a raise “because of taxes” is the wrong move

And all of this makes the upcoming capital gains discussion much easier—not to mention way more interesting. Long-term capital gains taxes have their own progressive brackets, including that lovely zero percent bracket.

If you found this post helpful, please leave a comment below (or share it with that one coworker who still thinks a higher bracket is a punishment).

See you at the finish line!

Disclaimer: I’m not a licensed financial professional. This blog shares my personal experiences and opinions around money, investing, and early retirement. It’s for informational and educational purposes only—not financial, legal, or tax advice. Always do your own research or consult with a qualified professional before making any financial decisions.

Comments