The Worst Credit Score Advice I Ever Received (And Why It Cost Me Points)

- Gin

- Jun 26

- 6 min read

I get an email every time my FICO credit score changes.

This week, I finally checked it for the first time in months.

847.

After years of hovering around 835, I was suddenly three points away from perfection.

Naturally, I ran to tell my wife because we're just competitive enough to compare credit scores.

Unfortunately for me, she's one of the fewer than 2% of Americans with a perfect 850, so I never win.

When I look at our credit scores, I think about the different “tips” we received when we were younger about how to pay our credit card balances. We were told they would improve our credit scores.

But guess what? We achieved our scores with just very basic and simple practices. No special hacks were needed because most of the popular tips actually hurt your score rather than improve it.

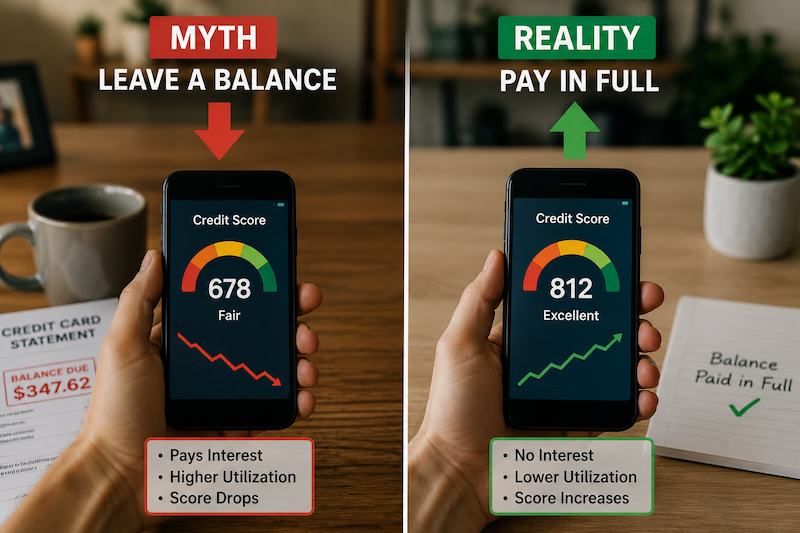

Especially the most popular misconception that never seems to die—that leaving a credit card balance improves your credit score.

THE MYTH OF LEAVING A CREDIT CARD BALANCE

I have friends who were given this advice by their parents, and I was told this by a mentor early on in my career as well.

Conventional wisdom says: “Never pay your credit card balance in full. Always leave a small balance remaining to improve your credit score.”

Too bad it’s flat-out wrong.

Your credit score takes a hit every time you don’t pay your balance in full. It doesn’t matter if you’re still paying the minimum amount due. Your score will go down. Period.

I know this from practice. I respected my mentor, so I took his advice. My score was already decent, but who doesn't want a higher number? So I followed his advice.

And I saw my score drop.

My spending habits hadn’t changed. Just how I paid my balance.

When I returned to paying my balance in full again, my score went back up. That was the only time I ever carried over a balance on any of my credit cards.

If you’ve been following this “advice” and wondering why your credit score hit a ceiling, you’re not alone. About 50% of Americans believe this advice.

WHY SO MANY PEOPLE STILL BELIEVE THIS

The misconception has been parroted for so long that many accept it as the truth. It’s like how some women still believe that shaving instead of waxing their legs will make their leg hair grow back thicker and darker than a sasquatch.

Total B.S. and thoroughly debunked.

Yet the myth about leaving a balance persists because of misconstrued logic and misunderstandings.

Myth #1: It shows you can responsibly manage credit

This was the reasoning explained to me, and it’s so dumb. That's like saying the person constantly fixing fender benders is a more responsible driver than the one who never crashes. Credit companies don’t reward you for paying interest.

Myth #2: You must have a balance to show your account is active

Yes, your credit score is based on recent activity. But no, carrying debt isn’t the same as having activity. Even making a small purchase each month and paying off the balance in full each time will count as activity. And you pay no interest!

Myth #3: You need to always have a small balance to show a low utilization rate

Credit bureaus love seeing you use as little of your total available credit as possible. But that doesn’t mean you need to constantly carry a balance to show how “little you’re using.” Credit card companies share your balance with credit bureaus only once a month at the statement closing date. So you can pay your balance in full each month and still show active usage.

Myth #4: Credit card companies reward you for making them money by paying interest

Uh, no. The credit bureaus determine your score, not the credit card companies. And they are separate entities. So yeah, credit card companies love it when you pay interest, but you get nothing for it.

WHAT ACTUALLY IMPROVES YOUR CREDIT SCORE

As mentioned, my wife and I didn’t use any tricks to get our 847 and 850 credit scores. We just did two simple things to show we were responsible credit users.

Two factors make up 65% of your score—your payment history and credit utilization ratio. And fortunately, you have a lot of control over them.

Here’s how to take advantage of that knowledge.

PAY BALANCES IN FULL EVERY TIME

A credit score is all about trust. The higher the number, the more trust you’ve earned. And your payment history determines 35% of your credit score.

Imagine you have two family members who are always borrowing money from you. One family member always pays you back in full on time. The other sometimes pays late and never pays you back in full. Maybe he spent all his cash, simply forgot, or just didn’t see it as a priority.

Which family member would you trust more and give a higher score to?

If you consistently pay in full and on time, your score will go up. It’s that simple.

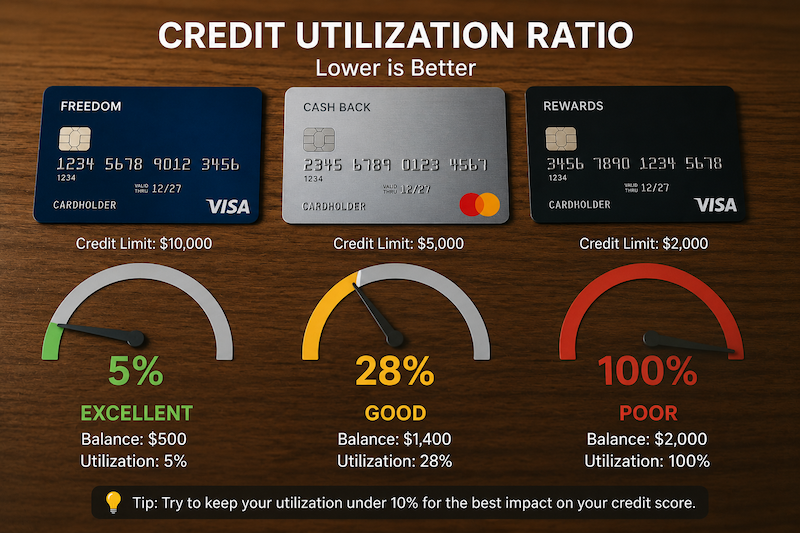

KEEP A LOW CREDIT UTILIZATION RATIO

Your credit utilization ratio refers to how much of your available credit you’re using and determines 35% of your credit score. Using less than 30% of your available credit is good, but keeping it under 10% is best.

The important thing to understand is that your credit utilization ratio doesn’t just apply to your total aggregate available credit but also to each credit card.

For example, imagine you have two credit cards with credit limits of $1,000 and $9,000. If you maxed out your $1,000 credit card, you would’ve only used 10% of your total aggregate credit, which is great. But your utilization ratio for that one card is 100%, which is horrible.

All this means is to pay attention to how you spread your credit usage across your credit cards.

INCREASE CREDIT LIMITS

OK, I know I promised only two tips. But technically, this one is just a sneaky extension of Tip #2.

Assuming the dollar amount of credit you use doesn’t change, one easy way to lower your utilization ratio is to increase the amount of credit you have. Using the previous example, if the $1,000 credit limit increased to $4,000, your utilization ratio for that card would be just 25% instead of 100%.

As a general rule, you can request a credit limit increase every 6 to 12 months per credit card account. I request an increase every year. I don’t need the additional credit, but I like seeing my utilization ratio drop lower and lower.

FREQUENTLY ASKED QUESTIONS

What is a Good Credit Score?

Anything below 670 is poor and needs work. A score of 670-739 is considered good, 740-799 is very good, and 800+ is exceptional. In reality, though, lenders don’t care if your score is above 760. After that score, lenders give no additional discounts or fee reductions.

What Happens When You Get a Perfect Credit Score

When you get an 850 score, the credit bureaus send you a plaque with your name on it.

Just kidding. You get nothing but bragging rights that are impossible to weave into a conversation naturally.

Other Than Payment History (35%) and Credit Utilization Ratio (30%), What Determines a Credit Score?

The length of your credit history or how long you’ve had credit determines 15% of your score. Your credit mix (mortgage, car loan, etc.) makes up 10% of your score. The final 10% of your score is determined by what new credit you have.

Why Pay Credit Card Balance in Full When I Don’t Do That for My Car Loan?

That’s an apples-to-oranges comparison. Credit cards don’t function the same as installment loans, like your car loan or mortgage.

STOP PAYING INTEREST FOR BAD ADVICE

There are people like finance guru Dave Ramsey who are totally against credit cards and debt in general.

But we can’t all buy cars and homes in all cash. And a credit score isn’t just for borrowing money. A good score can get you cheaper insurance rates, waive security deposits, and even help you secure an apartment.

It’s the primary way companies measure your financial responsibility, so aim to get it as high as possible.

My wife still reminds me that her 850 beats my 847 every chance she gets.

But here's the funny part: from a lender's perspective, there's essentially no difference. Once you're above roughly 760, you've already unlocked the best rates available.

So don't waste money paying interest because someone told you carrying a balance helps your score. It doesn't.

Instead, pay in full, pay on time, keep your utilization low, and let your score take care of itself.

And if you somehow reach a perfect 850, feel free to brag about it. Just don't expect a trophy.

See you at the finish line!

Disclaimer: I’m not a licensed financial professional. This blog shares my personal experiences and opinions around money, investing, and early retirement. It’s for informational and educational purposes only—not financial, legal, or tax advice. Always do your own research or consult with a qualified professional before making any financial decisions.

Comments